Introduction: Why Your CIBIL Score Matters More Than You Think

Have you ever faced this situation?

- You applied for a loan

- Your income is stable

- All documents are correct

👉 Still, your loan got rejected

The reason is often your CIBIL score.

Many people don’t realize that their credit score is calculated based on specific financial behaviors. If you don’t understand how your CIBIL score is calculated, you may unknowingly damage it.

In this guide, you’ll learn everything about:

- How a CIBIL score is calculated

- What factors affect it

- How to improve it step-by-step

Featured Snippet (Quick Answer)

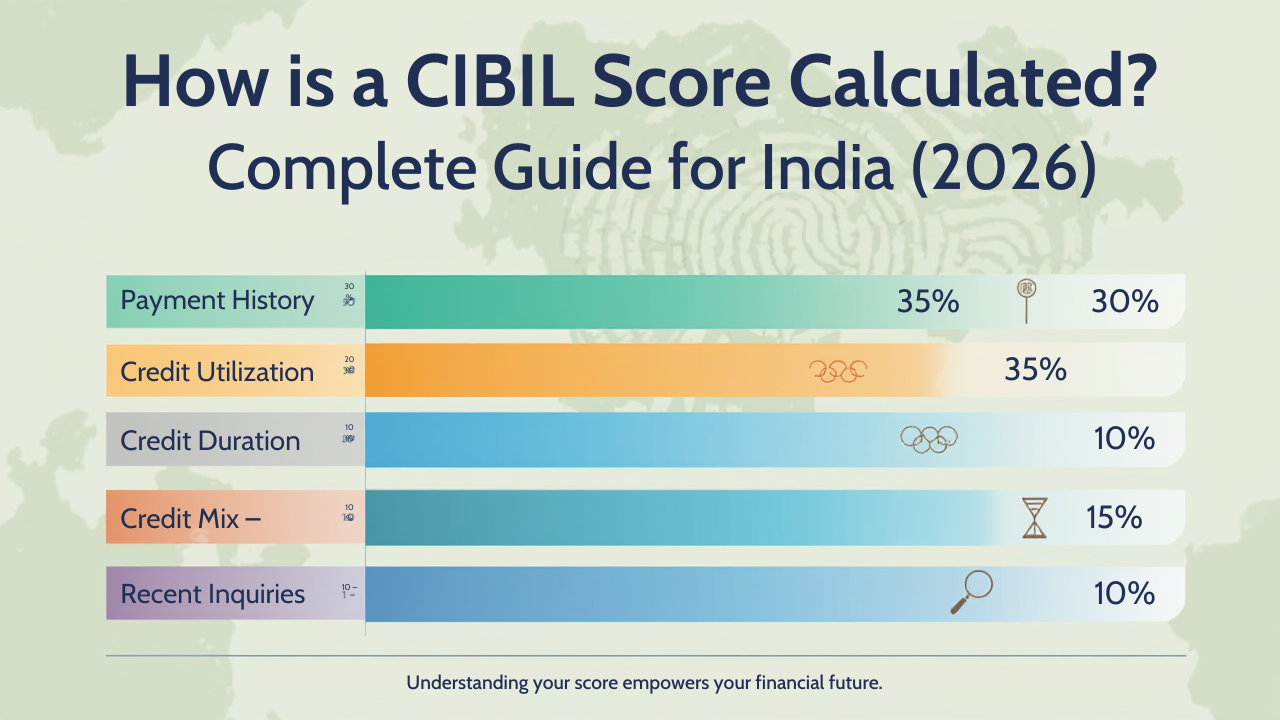

How is a CIBIL score calculated?

A CIBIL score is calculated based on five key factors:

- Payment History – 35%

- Credit Utilization – 30%

- Length of Credit History – 15%

- Credit Mix – 10%

- Credit Enquiries – 10%

What is CIBIL Score Calculation? (Simple Explanation)

A CIBIL score is a 3-digit number ranging from 300 to 900 that represents your creditworthiness.

It is calculated by TransUnion CIBIL using your financial data, such as:

- Loan repayment history

- Credit card usage

- Outstanding balances

- Past defaults

👉 In simple terms:

Your CIBIL score reflects how responsible you are with credit.

CIBIL Score Range in India

| Score Range | Meaning |

| 750 – 900 | Excellent |

| 650 – 750 | Average |

| Below 650 | Risky |

👉 A score above 750 significantly increases your chances of loan approval.

How is a CIBIL Score Calculated? (Detailed Breakdown)

1. Payment History (35%) – The Most Important Factor

This is the biggest contributor to your score.

It includes:

- Timely EMI payments

- Credit card bill payments

- Any missed or delayed payments

👉 Impact:

Even one missed payment can reduce your score significantly.

📌 Example:

If you miss 2 EMIs, your score can drop by 50–100 points.

2. Credit Utilization Ratio (30%)

This shows how much of your available credit you are using.

👉 Formula:

(Credit Used ÷ Total Credit Limit) × 100

📌 Example:

- Limit = ₹1,00,000

- Used = ₹80,000

- Utilization = 80% ❌

👉 Ideal usage: Below 30%

3. Length of Credit History (15%)

This measures how long you’ve been using credit.

- Older accounts = Positive impact

- New accounts = Limited impact

👉 A longer credit history builds trust with lenders.

4. Credit Mix (10%)

This refers to the types of credit you use:

- Secured loans (home loan, car loan)

- Unsecured loans (personal loan, credit card)

👉 A balanced mix improves your score.

5. Credit Enquiries (10%)

Whenever you apply for a loan or credit card, lenders check your CIBIL report.

👉 Each check = Hard enquiry

❌ Too many enquiries in a short time can lower your score.

Main Reasons That Affect CIBIL Score Calculation

- ❌ Late or missed payments

- ❌ High credit card usage

- ❌ Loan settlement instead of closure

- ❌ Multiple loan applications

- ❌ Written-off accounts

- ❌ Errors in credit report

Step-by-Step Guide to Improve Your CIBIL Score

Step 1: Check Your Credit Report

- Identify errors and discrepancies

- Verify all account details

Step 2: Maintain Payment Discipline

- Pay EMIs and credit card bills on time

- Avoid delays at all costs

Step 3: Reduce Credit Utilization

- Keep usage below 30%

- Avoid maxing out credit cards

Step 4: Keep Old Accounts Active

- Older accounts strengthen your credit profile

Step 5: Limit Loan Applications

- Avoid frequent credit enquiries

Step 6: Use Secured Credit

- Use FD-backed credit cards or small loans

Real-Life Example

Rohit had a CIBIL score of 590 due to:

- High credit card usage

- Late EMI payments

- Loan settlement

After taking corrective steps:

- Reduced credit usage

- Paid on time

- Fixed report errors

👉 His score improved to 730 within 6 months.

Common Mistakes to Avoid

🚫 Paying only minimum due

🚫 Using full credit limit

🚫 Settling loans instead of closing

🚫 Applying for multiple loans

🚫 Ignoring credit report

Expert Tips (Pro Insights)

✔ Enable auto-pay for all payments

✔ Maintain a low utilization ratio

✔ Check your credit report quarterly

✔ Use high-limit cards wisely

✔ Be cautious with joint loans

👉 Pro Tip:

If your score is already very low, professional help can speed up the improvement process.

FAQs (Frequently Asked Questions)

1. How often is the CIBIL score updated?

Usually monthly, when lenders update your data.

2. Does one missed EMI affect the score?

Yes, especially recent delays have a strong impact.

3. How long does it take to improve a CIBIL score?

Typically 3–6 months with consistent efforts.

4. Are multiple enquiries harmful?

Yes, especially within a short period.

5. Can I have a score without credit history?

No, you will be categorized as “No Credit History.”

Conclusion: Understand the Calculation, Take Control

Your CIBIL score is not random—it is calculated using clear, measurable factors.

If you understand and manage these 5 factors properly, you can:

- Improve your credit score

- Get loans easily

- Secure better interest rates

🚀 Call To Action (Take Action Now)

If your CIBIL score is low, your report has incorrect entries, or your loan is getting rejected, there’s no need to worry. CrediBoost Solutions Pvt. Ltd. helps you professionally analyze and improve your credit profile.

👉 Get your free consultation today and take control of your CIBIL score.

📞 Call/WhatsApp: 8099690448 / 7086962101

🌐 Website: crediboost.in

CIN Number – U66190AS2025PTC027785

Leave a Reply