Introduction: Do You Have a Low CIBIL Score?

If your loan has been rejected or a bank has offered you a high interest rate, the biggest reason could be:

👉 Low CIBIL Score

Many people don’t understand:

- What exactly is a low CIBIL score?

- What score is considered low?

- Most importantly — how to improve it?

👉 Reality:

A low CIBIL score means banks consider you a risky borrower.

In this guide, we will understand:

- What a low CIBIL score is

- Why it happens

- How to fix it

Featured Snippet (Quick Answer)

What is a low CIBIL score?

In India, a CIBIL score below 650 is considered low. At this score, loan approval becomes difficult and interest rates are higher.

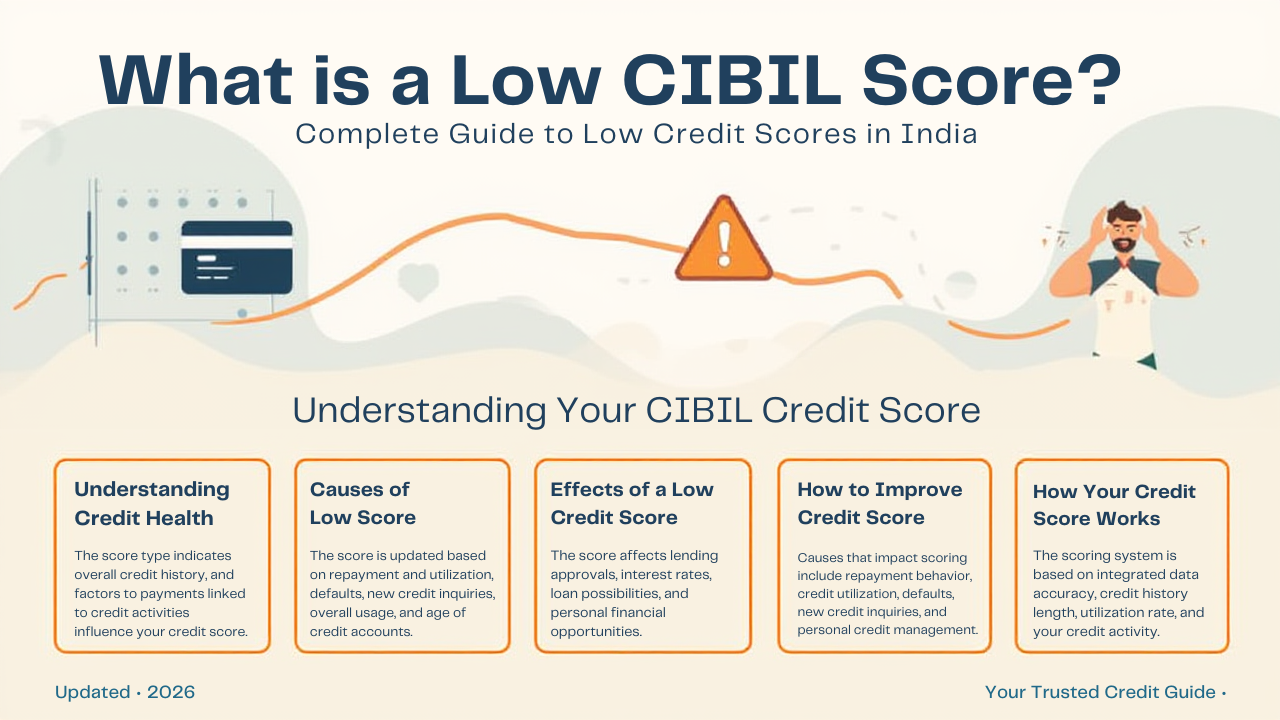

What is a Low CIBIL Score? (Simple Explanation)

A CIBIL score is a 3-digit number (300–900).

👉 Score categories:

- 750+ = Excellent

- 700–749 = Good

- 650–699 = Average

- Below 650 = Low / Poor ❌

👉 In simple words:

Low CIBIL score = Financial risk signal for banks

Why is a Low CIBIL Score a Problem?

With a low score, you may face:

- ❌ Loan rejection

- ❌ Higher interest rates

- ❌ Difficulty in credit card approval

- ❌ Lower credit limit

👉 Example:

- Score 780 → Loan @ 10%

- Score 600 → Loan @ 16%

👉 Huge financial loss!

Main Reasons for Low CIBIL Score

If your score is low, these could be common reasons:

- ❌ Late EMI or credit card payments

- ❌ Loan default or non-payment

- ❌ Loan settlement (not full payment)

- ❌ High credit card usage (80–100%)

- ❌ Multiple loan enquiries

- ❌ Written-off accounts

- ❌ Errors in credit report

👉 All these directly reduce your score.

How to Fix a Low CIBIL Score (Step-by-Step Guide)

Step 1: Check Your Credit Report

- Identify errors

- Verify all accounts

Step 2: Maintain Payment Discipline

- Pay EMIs and bills on time

- Enable auto-debit

Step 3: Reduce Credit Utilization

- Keep usage below 30%

📌 Example:

₹1,00,000 limit → Use ₹30,000

Step 4: Clear Outstanding Dues

- Pay pending amounts

- Do not ignore old dues

Step 5: Control Loan Applications

- Avoid frequent applications

Step 6: Use Secured Credit

- FD-based credit cards are helpful

Real-Life Example (Relatable Case)

Imran had a CIBIL score of 580.

Reason:

- Credit card overuse

- EMI delays

- One settled loan

He:

- Followed payment discipline

- Reduced utilization

- Corrected his report

👉 In 6 months, his score improved to 740

Common Mistakes to Avoid

🚫 Paying only minimum due

🚫 Settling loans

🚫 Using full credit limit

🚫 Missing EMIs

🚫 Ignoring credit report

Expert Tips (Pro Insights)

✔ Enable auto-pay

✔ Use high-limit cards with low usage

✔ Check report quarterly

✔ Keep old accounts active

👉 Pro Tip:

Professional guidance can significantly help in improving a low score faster.

FAQs (Frequently Asked Questions)

1. What is considered a low CIBIL score?

Below 650 is considered low.

2. Can I get a loan with a low score?

Yes, but with higher interest and difficult approval.

3. How long does it take to improve the score?

3–6 months with proper discipline.

4. Does loan settlement improve the score?

No, it further damages the score.

5. Does missing one EMI affect the score?

Yes, and the impact is significant.

Conclusion: A Low Score is Not Permanent

A low CIBIL score is a problem — but not permanent.

👉 With the right strategy, you can:

- Improve your score

- Get loan approvals

- Build a better financial life

👉 Golden Rule:

Discipline + Awareness = High CIBIL Score

🚀 Call To Action (Take Action Now)

If your CIBIL score is low, your report has incorrect entries, or your loan is getting rejected — there is no need to worry.

CrediBoost Solutions Pvt. Ltd. helps you professionally analyze and improve your credit profile.

👉 Get your free consultation today and improve your CIBIL score.

📞 Call/WhatsApp: 8099690448 / 7086962101

🌐 Website: crediboost.in

CIN Number – U66190AS2025PTC027785

Leave a Reply