Introduction: Is “DPD” Showing in Your Credit Report?

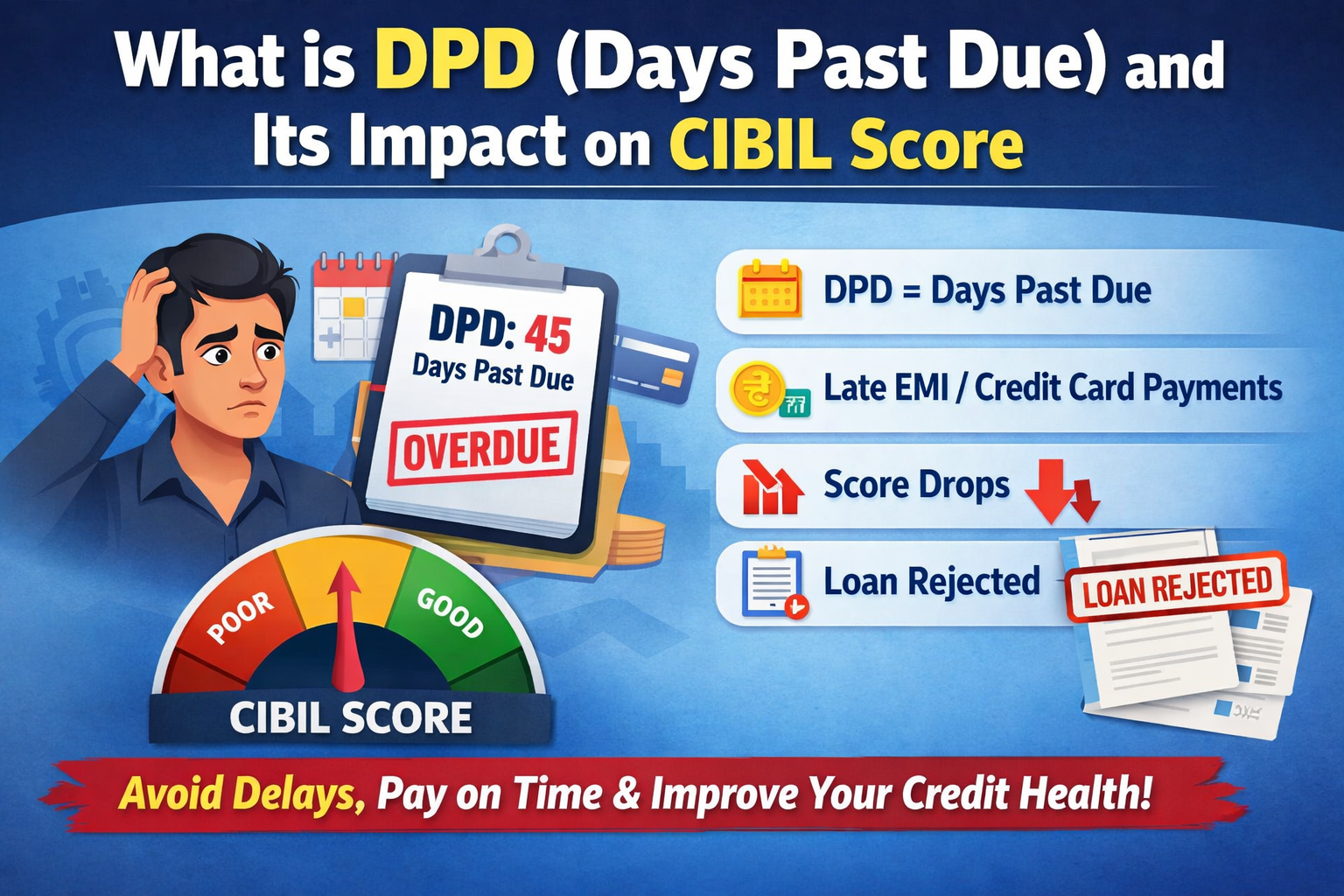

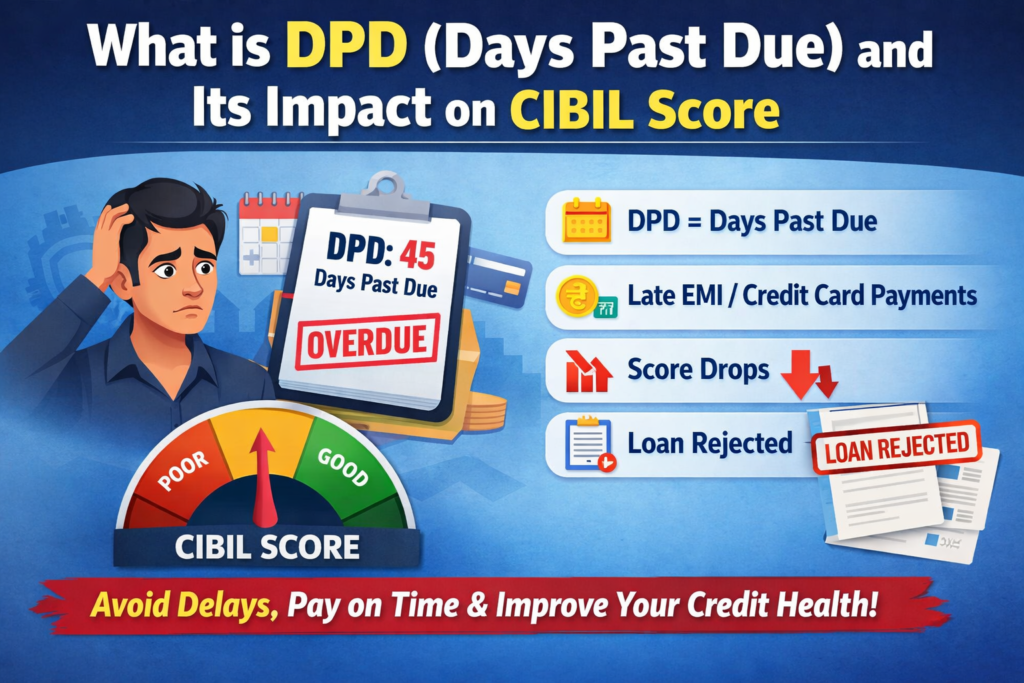

If you’ve checked your credit report, you’ve probably noticed the term DPD (Days Past Due). Many people ignore it or don’t fully understand its importance—but it is one of the most critical factors affecting your CIBIL score.

👉 DPD tells lenders how many days you delayed your EMI or credit card payment.

If your DPD is high:

- Your credit score drops

- Loan approvals become difficult

- Lenders consider you a risky borrower

In this guide, you’ll learn everything about DPD and how to manage it effectively.

📌 Featured Snippet (Quick Answer)

DPD (Days Past Due) refers to the number of days a borrower has delayed in making a payment after the due date. A higher DPD indicates poor repayment behavior and negatively impacts the CIBIL score.

What is DPD (Days Past Due)? (Simple Explanation)

DPD is a numeric indicator in your credit report that shows how late your payment was.

Example:

- Due Date: 5th March

- Payment Date: 15th March

👉 DPD = 10 days

How DPD Appears in CIBIL Report

DPD values are shown in codes like:

- 000 → Payment made on time (Best)

- 030 → 30 days late

- 060 → 60 days late

- 090 → 90 days late

- XXX → No data or no activity

👉 30+ DPD is a warning

👉 90+ DPD is considered a serious default

Main Reasons / Causes of High DPD

Here are common reasons why DPD increases:

- Missing EMI due dates

- Financial difficulties (job loss, emergency)

- Ignoring credit card payments

- Too many active loans

- Poor financial planning

- Auto-debit failures

Impact of DPD on CIBIL Score

DPD reflects your repayment discipline, and lenders pay close attention to it.

🔴 Negative Impact:

- 30+ DPD → Score starts dropping

- 60+ DPD → Significant negative impact

- 90+ DPD → High-risk borrower classification

👉 Repeated delays can:

- Lead to loan rejection

- Increase interest rates

Real-Life Example

Priya, a salaried employee, had a personal loan.

- She occasionally delayed EMIs

- Her report showed multiple “030” entries

👉 Result:

- Credit score dropped from 780 to 680

- Home loan application was rejected

Solutions / Actionable Steps (Step-by-Step)

If your DPD is high, follow these steps:

Step 1: Check Your Credit Report

- Identify where delays occurred

Step 2: Clear Outstanding Dues

- Pay all pending EMIs and credit card bills

Step 3: Enable Auto-Debit

- Avoid missing due dates

Step 4: Set Payment Reminders

- Get alerts before due dates

Step 5: Control Credit Utilization

- Keep it below 30%

Step 6: Build Positive Payment History

- Make all payments on time consistently

Common Mistakes to Avoid

- Ignoring EMI payments

- Paying only minimum due on credit cards

- Not checking your credit report

- Taking too many loans

- Forgetting due dates

Expert Tips / Pro Insights

- Always pay before the due date

- Maintain an emergency fund (3–6 months expenses)

- Use auto-debit and reminders

- Pay full credit card dues

- Monitor your credit report regularly

👉 Pro Tip:

Even a single 30+ DPD can impact your score—consistency is key.

FAQs (Frequently Asked Questions)

1. What does DPD stand for?

Days Past Due — number of days a payment is delayed.

2. Does a 1–2 day delay affect the score?

Minor impact, but repeated delays can harm your score.

3. Can DPD be removed?

Only if it is an error; otherwise, it remains as payment history.

4. What is a safe DPD?

000 (on-time payment) is ideal.

5. How long does DPD stay in the report?

Typically up to 36 months (3 years).

Conclusion: Small Delays, Big Consequences

DPD may look like a small number, but it has a big impact on your credit health.

👉 By maintaining discipline:

- Your credit score improves

- Loan approvals become easier

- Financial stability increases

Timely payments are the foundation of a strong credit profile.

🚀 Call-To-Action

If your CIBIL score is low, your report has incorrect entries, or your loan applications are getting rejected, there’s no need to worry. CrediBoost Solutions Pvt. Ltd. helps you professionally analyze and improve your credit profile.

✔ Expert analysis

✔ Personalized solutions

✔ Fast-track credit improvement strategies

👉 Get your FREE consultation today and start improving your CIBIL score now.

📞 Call/WhatsApp: 8099690448 / 7086962101

🌐 Website: crediboost.com

Contact Number – 8099690448 / 7086962101

Address – C/O Sri Nagendra Borma, Hatilong, Near Maruti Suzuki Arena, North Lakhimpur, Assam – 787031

Email – support@crediboost.in

CIN NUMBER – U66190AS2025PTC0277857

Don’t wait—start improving your credit score today! 🚀