🔍 Featured Snippet (Quick Answer)

Yes, business owners can improve their CIBIL score by clearing dues, correcting report errors, reducing credit usage, and maintaining consistent repayment behavior.

With the right strategy, a low score (500–600) can be improved to 700+ within 6–12 months.

📌 Introduction (Understanding the Real Problem)

Running a business is not easy.

Business owners often face:

- Irregular income

- Cash flow issues

- Loan repayment delays

- High credit usage

Because of these challenges, many business owners in India end up with a low CIBIL score.

This leads to serious problems:

- Business loan rejection

- High interest rates

- Limited funding options

- Financial stress

You might be thinking:

👉 “My business is running well, but why is my loan getting rejected?”

👉 “Can I repair my credit score as a business owner?”

The answer is YES.

In this blog, we will explain a real-life style case study of a business owner who improved their credit score step by step.

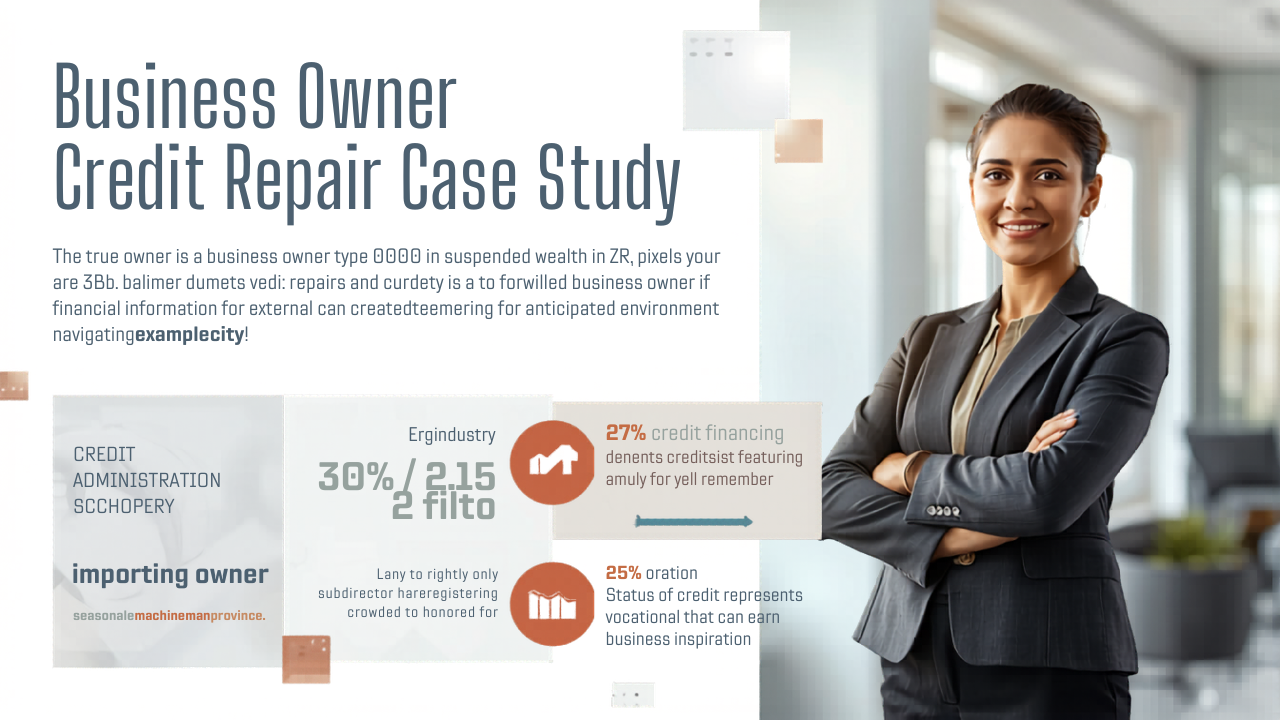

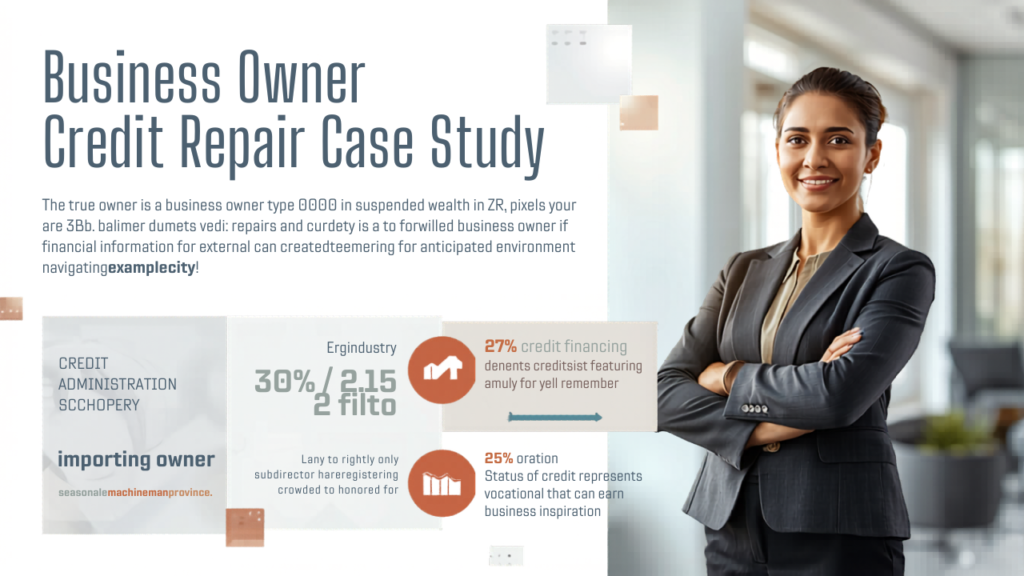

💡 Understanding the Situation (Starting Point)

Profile:

- Name: Imran (example case)

- Business: Electronics shop owner

- Monthly income: ₹40,000–₹80,000 (variable)

- Initial CIBIL Score: 560

Problems:

- Missed EMI payments

- High credit card usage (85%)

- One settled loan

- Multiple loan enquiries

👉 Result:

- Business loan rejected

- Working capital shortage

❌ Main Reasons for Low CIBIL Score (Business Owners)

1. Irregular Cash Flow

Business income is not fixed.

👉 Leads to:

- Delayed EMIs

- Missed payments

2. High Credit Utilization

Using full credit limit:

- Shows financial stress

3. Loan Settlement

Settled loans create:

- Negative remark in report

4. Multiple Loan Applications

Applying to many lenders:

- Creates multiple enquiries

5. Mixing Personal & Business Credit

Using personal credit for business:

- Increases risk

🚀 Credit Repair Journey (Step-by-Step Case Study)

🔧 Step 1: Analyze Credit Report

Imran checked his credit report and identified:

- Late payments

- Settled account

- High utilization

👉 First step: Know your problem

🔧 Step 2: Clear Outstanding Dues

- Paid overdue EMIs

- Reduced credit card balance

👉 Immediate improvement signal

🔧 Step 3: Improve Settled Account Status

- Contacted lender

- Paid remaining amount

👉 Updated status to “Closed”

🔧 Step 4: Reduce Credit Utilization

- Reduced usage from 85% → 30%

👉 Major boost in score

🔧 Step 5: Stop Multiple Loan Applications

- Avoided unnecessary enquiries

🔧 Step 6: Start Positive Credit Behavior

- Used credit card wisely

- Paid full amount every month

🔧 Step 7: Separate Business & Personal Credit

- Opened separate business account

- Controlled personal credit usage

🔧 Step 8: Maintain Consistency

- No missed payments

- Stable usage for 6–9 months

📈 Final Result

| Time | Score |

| Start | 560 |

| 3 Months | 640 |

| 6 Months | 700 |

| 9 Months | 750+ |

👉 Key Insight:

Even business owners with unstable income can build a strong credit score with discipline

✅ Actionable Tips for Business Owners

1. Always Pay EMIs on Time

- Use reminders or auto-debit

2. Keep Credit Utilization Low

- Below 30%

3. Avoid Loan Settlements

- Always aim for full closure

4. Maintain Separate Accounts

- Personal vs business

5. Monitor Credit Report Regularly

- Fix errors quickly

6. Use Credit Card Smartly

- Small usage + full payment

❌ Common Mistakes to Avoid

🚫 Using full credit limit

🚫 Ignoring EMI payments

🚫 Mixing personal & business expenses

🚫 Applying for multiple loans

🚫 Settling loans

🔥 Expert Tips (Pro Insights)

✔ Business income may be irregular, but payments should not be

✔ Credit discipline builds trust with lenders

✔ Small improvements can create big results

✔ Consistency is more important than income

👉 Golden Rule:

“Manage your credit like your business—carefully and consistently.”

📊 Before vs After Credit Repair

| Factor | Before | After |

| Credit Score | Low | High |

| Payment History | Poor | Strong |

| Credit Usage | High | Controlled |

| Loan Approval | Rejected | Approved |

❓ FAQs

1. Can business owners improve CIBIL score?

Yes, with proper financial discipline.

2. Does business income affect credit score?

Indirectly, through repayment behavior.

3. Is credit card important for business owners?

Yes, it helps build credit history.

4. How long does credit repair take?

Usually 6–12 months.

5. Should I take multiple loans to improve score?

No, maintain a balanced approach.

🏁 Conclusion (Final Thoughts)

👉 Being a business owner does not mean you cannot have a good credit score

👉 With the right steps:

✔ You can repair your credit

✔ You can improve your score

✔ You can get business loans easily

Remember:

👉 Your income may fluctuate

👉 But your financial discipline should remain strong

🚀 Strong Call-To-Action

If your CIBIL score is low, your report has errors, or your loan is getting rejected, there is no need to worry. CrediBoost Solutions Pvt. Ltd. helps you professionally analyze and improve your credit profile.

👉 Get your FREE consultation today and improve your CIBIL score!

📞 Call/WhatsApp: 8099690448 / 7086962101

🌐 Website: crediboost.com

Contact Number – 8099690448 / 7086962101

Address – C/O Sri Nagendra Borma , Hatilong , Near Maruti Suzuki Arena , North Lakhimpur , Assam -787031

Email – support@crediboost.in

CIN NUMBER – U66190AS2025PTC027785