Introduction: Is Your Loan “Closed” or Just “Settled”?

Many people in India take loans or use credit cards, but when repayment issues arise, two terms often create confusion — “Settled” and “Closed.”

Most borrowers think:

👉 “Settlement means loan is finished”

👉 “Closed and Settled are the same thing”

But the truth is — these two statuses have a huge impact on your CIBIL score and future loan eligibility.

If you have ever settled a loan or are planning to do so, this guide will help you make the right decision.

📌 Featured Snippet (Quick Answer)

A Closed Account means you have repaid your loan in full — this improves your credit score.

A Settled Account means you paid only a part of the loan after negotiation — this negatively affects your CIBIL score and reduces your chances of getting future loans.

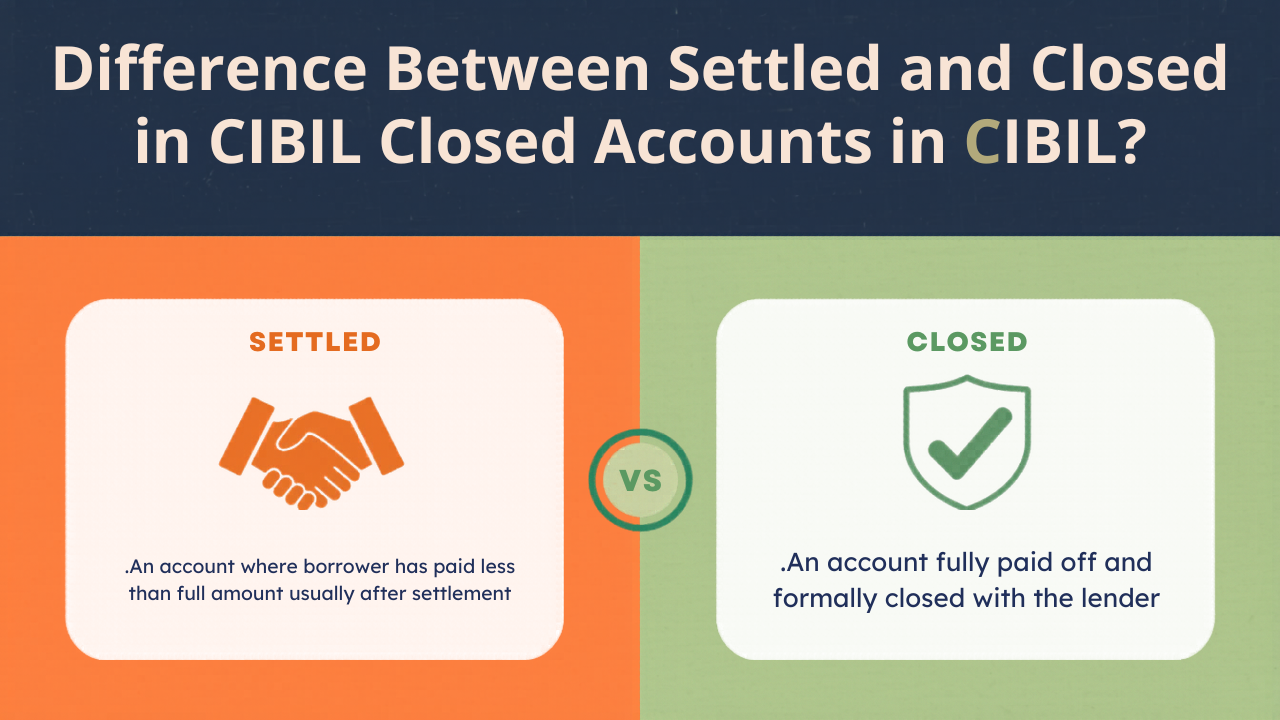

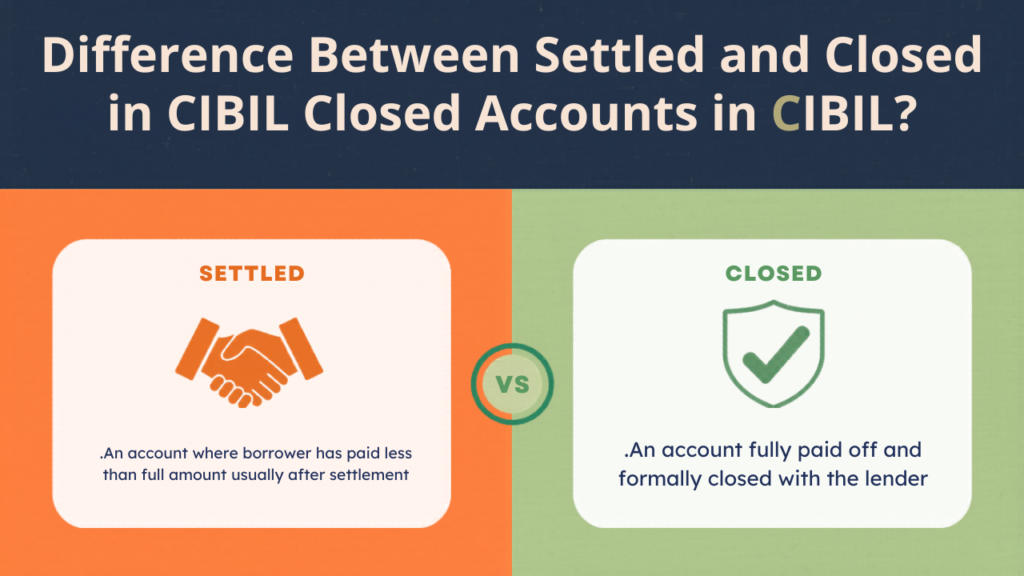

What is a Closed Account in CIBIL?

A Closed Account is when a borrower successfully repays the entire loan amount along with interest, as per the agreed terms.

Example:

You take a personal loan of ₹2,00,000 and repay all EMIs on time until completion.

👉 Result:

- Status: Closed

- Impact: Positive

- Credit Score: Improves

What is a Settled Account in CIBIL?

A Settled Account is when a borrower is unable to repay the full loan amount and negotiates with the lender to pay a reduced amount.

Example:

Your outstanding loan is ₹1,00,000, but you negotiate and pay ₹60,000 as a final settlement.

👉 Result:

- Status: Settled

- Impact: Negative

- Credit Score: Drops

Key Differences Between Settled and Closed Accounts

| Factor | Closed Account | Settled Account |

| Payment | Full repayment | Partial repayment |

| Credit Score Impact | Positive | Negative |

| Loan Approval | Easier | Difficult |

| Lender Trust | High | Low |

| Credit History | Strong | Weak |

Main Reasons Why Accounts Get Settled

Here are the most common reasons why borrowers choose settlement:

- Financial crisis (job loss or business loss)

- High debt burden

- Medical or emergency expenses

- Poor financial planning

- Multiple loan defaults

- Irregular income

Impact on Your CIBIL Score

🔵 Closed Account:

- Builds a strong credit history

- Improves your credit score

- Increases chances of loan approval

🔴 Settled Account:

- Can reduce your score by 50–150 points

- Makes lenders consider you high-risk

- Reduces chances of future loan approvals

👉 This status can remain in your credit report for up to 7 years

Real-Life Example

Let’s understand with a simple case:

- Amit repaid his loan fully → Account Closed → Score: 780

- Rahul opted for settlement → Account Settled → Score: 620

👉 Result:

- Amit easily got another loan

- Rahul faced multiple rejections

Solutions / Actionable Steps (Step-by-Step)

If your account is marked as “Settled,” don’t worry—you can still improve your credit profile.

Step 1: Check Your Credit Report

- Identify all “Settled” accounts

Step 2: Repay Remaining Dues

- Contact your lender

- Clear the pending amount (if possible)

Step 3: Request Status Upgrade

- Ask the lender to update status from “Settled” to “Closed”

Step 4: Collect NOC

- Always get a No Objection Certificate after payment

Step 5: Build Positive Credit Behavior

- Use a secured credit card

- Pay EMIs and bills on time

- Maintain low credit utilization

Step 6: Monitor Your Credit Regularly

- Track your report and score consistently

Common Mistakes to Avoid

- Assuming settlement is a smart financial decision

- Not collecting NOC after payment

- Ignoring credit report updates

- Taking multiple loans simultaneously

- Repeating the same financial mistakes

Expert Tips / Pro Insights

- Always prioritize full repayment over settlement

- Use settlement only as a last option

- Keep your credit utilization below 30%

- Maintain an emergency fund (3–6 months expenses)

- Regularly monitor your credit report

👉 Pro Tip:

If you already have a settled account, try to upgrade it to “Closed” to rebuild your credit faster.

FAQs (Frequently Asked Questions)

1. Can a settled account be converted to closed?

Yes, if you repay the remaining amount and request the lender.

2. Is settlement a good option?

Only in extreme situations. It negatively impacts your credit score.

3. Which is better: settled or closed?

Closed account is always better.

4. How long does settled status stay in CIBIL?

Up to 7 years.

5. Can I get a loan after settlement?

It is difficult, but possible after improving your credit profile.

Conclusion: Make Smart Financial Decisions

Understanding the difference between Settled and Closed accounts is crucial for your financial future.

👉 Remember:

- Closed = Strong Credit Profile + Easy Loan Approval

- Settled = Weak Credit Profile + Loan Rejection Risk

Always aim to close your loans properly to maintain a healthy credit score.

🚀 Call-To-Action

If your CIBIL score is low, your report has incorrect entries, or your loan applications are getting rejected, there’s no need to worry. CrediBoost Solutions Pvt. Ltd. helps you professionally analyze and improve your credit profile.

✔ Expert analysis

✔ Personalized solutions

✔ Fast-track credit improvement strategies

👉 Get your FREE consultation today and start improving your CIBIL score now.

📞 Call/WhatsApp: 8099690448 / 7086962101

🌐 Website: crediboost.com

Contact Number – 8099690448 / 7086962101

Address – C/O Sri Nagendra Borma, Hatilong, Near Maruti Suzuki Arena, North Lakhimpur, Assam – 787031

Email – support@crediboost.in

CIN NUMBER – U66190AS2025PTC027785

Don’t wait—take control of your financial future today! 🚀