🔍 Featured Snippet (Quick Answer)

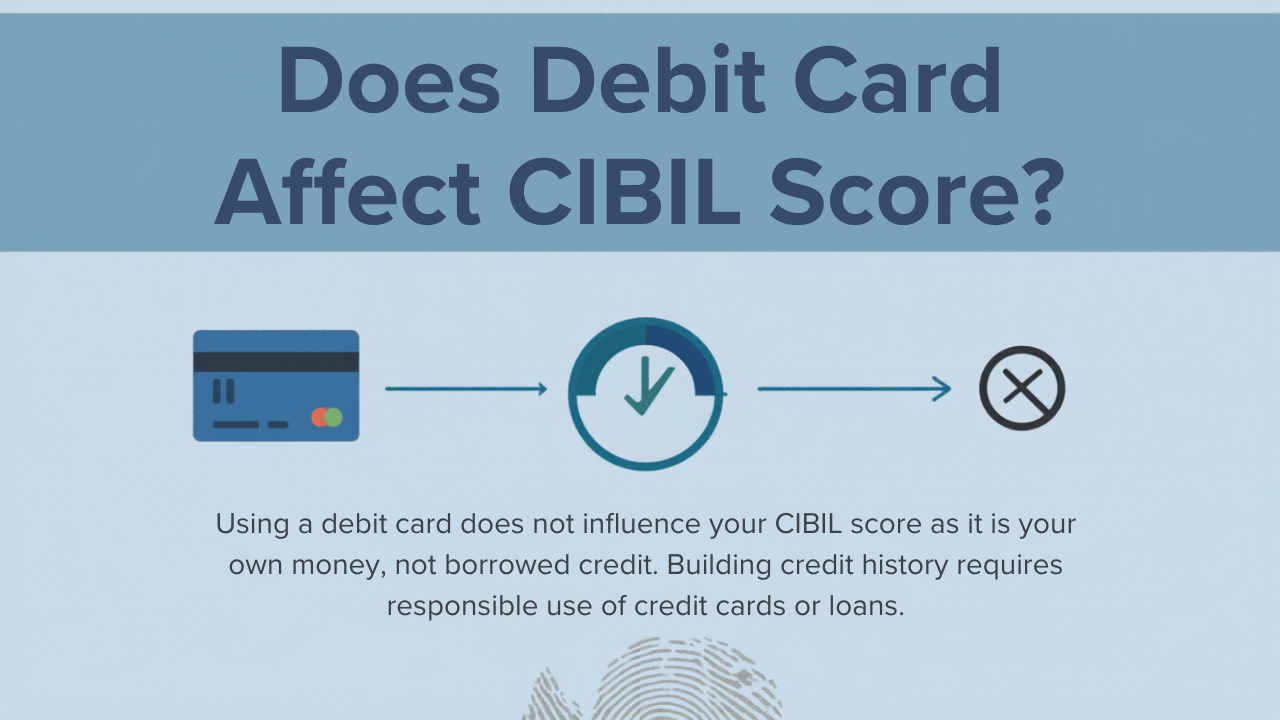

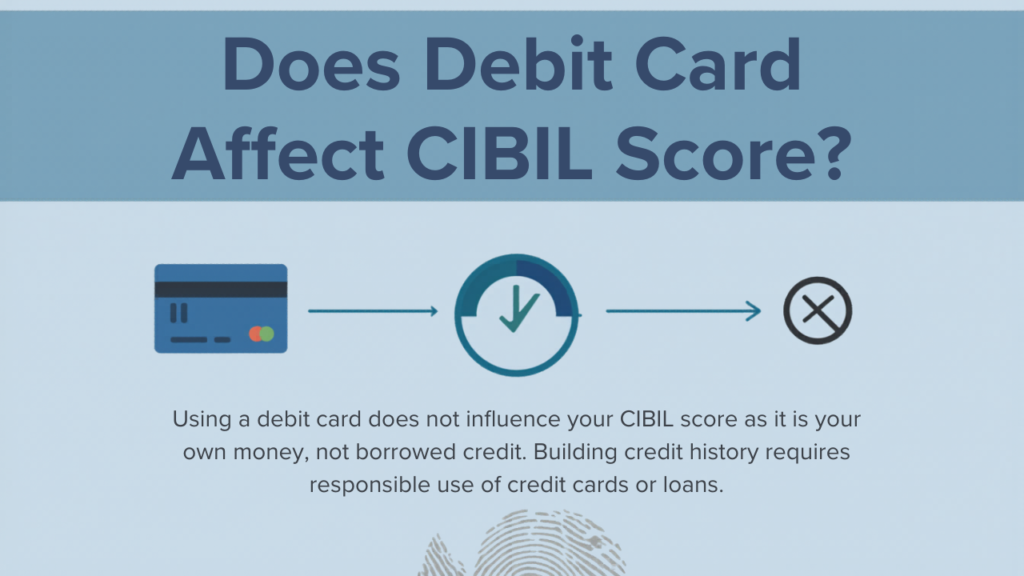

No, a debit card does NOT directly affect your CIBIL score.

Because a debit card uses your own money from your bank account, it does not involve any credit or borrowing.

However, your overall financial habits while using a debit card can indirectly influence your future creditworthiness.

📌 Introduction (Understand the Real Problem)

In today’s digital world, almost everyone uses a debit card for daily expenses—shopping, bill payments, ATM withdrawals, etc.

But a very common question people ask is:

👉 “Does using a debit card improve or reduce my CIBIL score?”

Many people believe:

- More debit card usage = better credit score

- ATM withdrawals impact credit score

- Digital payments help build credit

But the truth is different.

If you are planning to take a loan, credit card, or facing loan rejection, then understanding this topic is very important.

💳 What is a Debit Card? (Simple Explanation)

A debit card is a payment tool directly linked to your bank account.

👉 Whenever you use a debit card:

- Money is instantly deducted from your account

- No borrowing is involved

Example:

If your account has ₹10,000 and you spend ₹2,000 → your balance becomes ₹8,000

👉 Since there is no credit involved, it has no direct role in your CIBIL score.

📊 What is a CIBIL Score? (Basic Understanding)

A CIBIL score is a 3-digit number (300–900) that represents your creditworthiness.

👉 It helps lenders decide:

- Whether to approve your loan

- Interest rate you will get

- Credit card eligibility

Factors that affect your CIBIL score:

- Loan repayment history

- Credit card usage

- EMI payment behavior

- Credit utilization ratio

- Credit mix

👉 Notice: Debit card is NOT included in these factors

❌ Does Debit Card Directly Affect CIBIL Score?

Simple Answer: NO

👉 Because:

- It is not a loan

- No EMI is involved

- No credit limit exists

So:

✅ Debit card transactions are NOT reported to CIBIL

✅ It does NOT appear in your credit report

✅ It does NOT increase or decrease your score

⚠️ Indirect Impact of Debit Card (Important Insight)

Although debit cards don’t directly affect your score, they can indirectly influence your financial behavior, which matters for your credit score.

1. Poor Spending Habits

If you overspend using your debit card:

- Savings reduce

- Financial discipline weakens

👉 This may lead to missed EMIs in future → Score decreases

2. No Emergency Fund

If you depend only on your debit card and don’t save money:

- You may struggle during emergencies

- You may default on loans

👉 Result: Negative impact on CIBIL score

3. No Credit History

Using only a debit card:

❌ Does NOT build credit history

👉 This leads to:

- “No Score” or “Low Score”

- Loan rejection

4. No Proof of Creditworthiness

Banks cannot track:

- Your repayment behavior

- Your credit discipline

👉 So lenders hesitate to give loans

💡 Real-Life Example (Relatable Case Study)

Case 1: Rahul

- Uses only debit card

- No credit card or loan history

👉 Applies for loan → Rejected (No credit history)

Case 2: Amit

- Uses debit card + credit card

- Pays credit card bills on time

👉 Applies for loan → Approved (Good CIBIL score)

✅ Solutions: How to Improve Your CIBIL Score

If you are only using a debit card, follow these steps:

Step 1: Start Using a Credit Card

- Take a low-limit card

- Use it regularly

- Pay full bill on time

👉 Best way to build credit score

Step 2: Take Small Loans (If Needed)

- Consumer durable loans

- EMI purchases

👉 Timely repayment boosts score

Step 3: Never Miss EMI or Due Date

Even one missed payment can damage your score.

Step 4: Maintain Low Credit Utilization

- Use less than 30% of your credit limit

Step 5: Check Your CIBIL Report Regularly

- Identify errors

- Detect fraud

- Monitor improvement

❌ Common Mistakes to Avoid

🚫 Using only debit card forever

🚫 Not building credit history

🚫 Paying only minimum due

🚫 Missing EMI payments

🚫 Applying for multiple loans at once

🔥 Expert Tips (Pro Insights)

✔ Debit card is safe but doesn’t build credit

✔ Credit card is essential for credit score

✔ No credit history = Risky for lenders

✔ Smart users maintain a balance of both

👉 Best strategy:

Use debit card for daily expenses + credit card for building score

📊 Debit Card vs Credit Card

| Feature | Debit Card | Credit Card |

| Money Source | Your own money | Borrowed money |

| Impact on CIBIL | ❌ No | ✅ Yes |

| Builds Credit History | ❌ No | ✅ Yes |

| EMI Facility | ❌ No | ✅ Yes |

❓ FAQs

1. Does ATM withdrawal affect CIBIL score?

No, ATM withdrawals have no impact.

2. Can debit card usage improve credit score?

No, it does not improve your score.

3. Is debit card shown in CIBIL report?

No, it is not included.

4. Can I get a loan with only a debit card?

Possible, but difficult due to lack of credit history.

5. Which is better: Debit or Credit Card?

Both are useful, but credit cards help build your CIBIL score.

🏁 Conclusion (Final Thoughts)

👉 Debit card is a useful financial tool

👉 But it has no direct impact on your CIBIL score

If you only use a debit card:

- Your credit score may not grow

- Loan approval may become difficult

👉 The smart approach:

✔ Use debit card for spending

✔ Use credit card responsibly to build score

🚀 Strong Call-To-Action

If your CIBIL score is low, your report has errors, or your loan is getting rejected, there is no need to worry. CrediBoost Solutions Pvt. Ltd. helps you professionally analyze and improve your credit profile.

👉 Get your FREE consultation today and take control of your financial future!

📞 Call/WhatsApp: 8099690448 / 7086962101

🌐 Website: crediboost.com

Contact Number – 8099690448 / 7086962101

Address – C/O Sri Nagendra Borma , Hatilong , Near Maruti Suzuki Arena , North Lakhimpur , Assam -787031

Email – support@crediboost.in

CIN NUMBER – U66190AS2025PTC027785