🔍 Featured Snippet (Quick Answer)

Wrong entries in your credit report can reduce your CIBIL score, but they can be fixed by identifying errors, raising disputes, and following up with lenders.

Most corrections are updated within 30–45 days, and your score can improve significantly after fixing them.

📌 Introduction (Understanding the Real Problem)

Many people in India face loan rejection even when they have paid their dues on time.

The reason is often shocking:

👉 Wrong entries in their credit report

You may be facing issues like:

- Unknown loan showing in your report

- Paid loan still marked as “active”

- Closed account showing “written-off”

- Duplicate loan entries

These errors can seriously damage your CIBIL score and affect your financial life.

You might be thinking:

👉 “Why is my score low even after paying everything?”

👉 “How do I fix wrong entries in my credit report?”

This blog will explain everything through a real-life case study and give you a step-by-step solution.

💡 What is a Credit Report? (Simple Explanation)

A credit report is a detailed record of your loan and credit history.

It includes:

- Personal details

- Loan accounts

- Credit card usage

- Payment history

- CIBIL score

👉 Banks use this report to decide whether to give you a loan.

❌ What Are Wrong Entries in Credit Report?

Wrong entries are incorrect or outdated information in your credit report.

Common Examples:

- Loan you never took

- Closed loan showing as active

- “Settled” instead of “Closed”

- Wrong overdue amount

- Duplicate accounts

👉 Even one wrong entry can reduce your score significantly.

💡 Real-Life Case Study

Profile:

- Name: Suman (example)

- Salary: ₹25,000/month

- CIBIL Score: 580

Problem:

- Personal loan already paid

- Still showing as “Written-off”

- One unknown loan account

👉 Result:

- Loan rejected

- Credit card declined

🚀 Step-by-Step Fixing Process (Real Journey)

🔧 Step 1: Check Credit Report

Suman downloaded her credit report and found:

- Incorrect loan status

- Unknown account

👉 First step: Identify the problem

🔧 Step 2: Collect Proof

She gathered:

- Loan closure receipt

- Bank statements

- NOC (No Objection Certificate)

👉 Proof is very important

🔧 Step 3: Raise Dispute

- Submitted dispute to CIBIL

- Selected incorrect account

- Explained the issue clearly

🔧 Step 4: Contact Lender

- Sent email to bank

- Attached proof

- Requested correction

🔧 Step 5: Follow Up Regularly

- Checked status every week

- Followed up until resolved

🔧 Step 6: Wait for Update

After 30 days:

- Status changed from “Written-off” to “Closed”

- Unknown account removed

📈 Final Result

| Stage | Score |

| Before | 580 |

| After Correction | 700+ |

👉 Lesson:

Fixing errors can give fast and major improvement

⚠️ Main Reasons for Wrong Entries

1. Bank Reporting Errors

- Incorrect data submission

2. Technical Issues

- System glitches

3. Identity Mix-Up

- Same name / PAN confusion

4. Delay in Update

- Loan closed but not updated

5. Fraud or Unauthorized Loans

- Someone used your details

✅ Solutions: How to Fix Wrong Entries

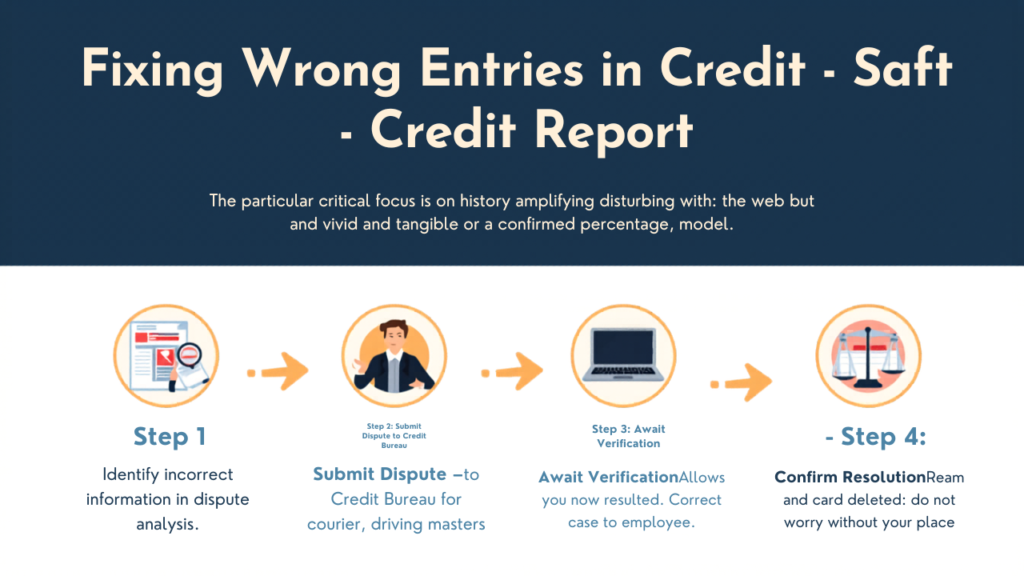

Step 1: Download Your Credit Report

- Check all details carefully

Step 2: Identify Errors

- Look for incorrect entries

Step 3: Raise Dispute with CIBIL

- Online dispute form

Step 4: Contact Bank/NBFC

- Send email with proof

Step 5: Attach Documents

- NOC

- Payment proof

- ID proof

Step 6: Follow Up

- Don’t ignore after raising dispute

Step 7: Check Updated Report

- Confirm correction

❌ Common Mistakes to Avoid

🚫 Ignoring credit report

🚫 Not keeping proof

🚫 Raising incomplete dispute

🚫 Not following up

🚫 Assuming bank will fix automatically

🔥 Expert Tips (Pro Insights)

✔ Check your credit report every 3 months

✔ Keep all loan documents safe

✔ Fix errors quickly before applying for loan

✔ Even small mistakes can reduce your score

👉 Golden Rule:

“Your credit report must always reflect correct information.”

📊 Before vs After Fixing Errors

| Factor | Before | After |

| Credit Score | Low | High |

| Loan Approval | Rejected | Approved |

| Report Accuracy | Wrong | Correct |

❓ FAQs

1. How long does it take to fix errors?

Usually 30–45 days.

2. Can wrong entries reduce score?

Yes, significantly.

3. Is dispute free?

Yes, CIBIL dispute process is free.

4. Can I fix report without bank?

Sometimes, but bank involvement is often required.

5. How often should I check report?

At least every 3 months.

🏁 Conclusion (Final Thoughts)

👉 Wrong entries can damage your financial future

👉 But they can be fixed with proper steps

✔ Check regularly

✔ Act quickly

✔ Keep proof

Remember:

👉 Your credit report should always be accurate

👉 Fixing errors can instantly improve your score

🚀 Strong Call-To-Action

If your CIBIL score is low, your report has errors, or your loan is getting rejected, there is no need to worry. CrediBoost Solutions Pvt. Ltd. helps you professionally analyze and improve your credit profile.

👉 Get your FREE consultation today and improve your CIBIL score!

📞 Call/WhatsApp: 8099690448 / 7086962101

🌐 Website: crediboost.com

Contact Number – 8099690448 / 7086962101

Address – C/O Sri Nagendra Borma , Hatilong , Near Maruti Suzuki Arena , North Lakhimpur , Assam -787031

Email – support@crediboost.in

CIN NUMBER – U66190AS2025PTC027785