📌 Quick Answer (Featured Snippet)

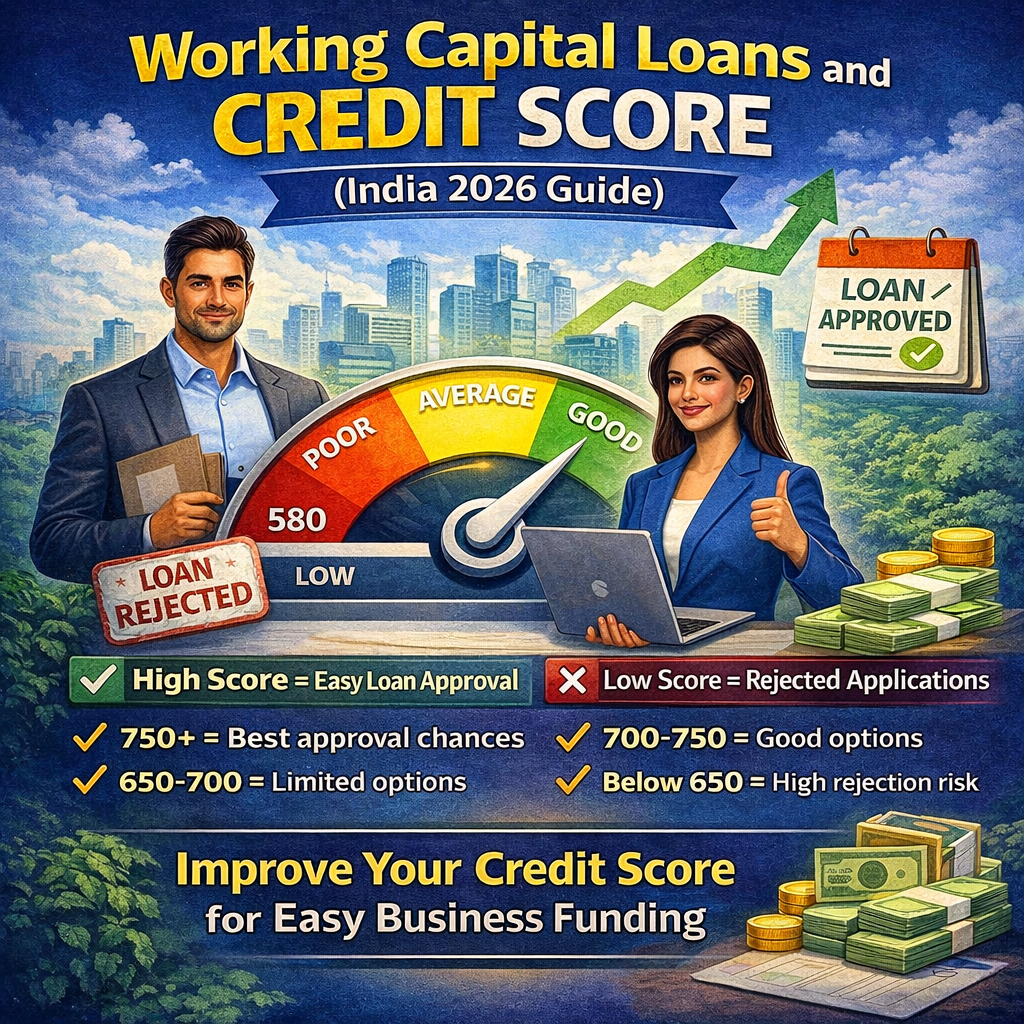

The minimum CIBIL score required for a business loan in India is generally 700 or above.

- 750+ → Excellent approval chances with low interest rates

- 700–750 → Good chances of approval

- 650–700 → Limited approval, higher interest

- Below 650 → Difficult to get approval

📖 Introduction – Facing Business Loan Rejections?

In today’s competitive market, whether you want to expand your business, manage working capital, or start a new venture — funding is essential.

But many entrepreneurs face a common issue:

👉 “My business loan got rejected”

👉 “Bank says my CIBIL score is low”

If you’re dealing with the same problem, this guide will help you understand everything clearly.

In this blog, you’ll learn:

✔ Minimum CIBIL score required for business loans

✔ Key factors banks consider

✔ Reasons for low CIBIL score

✔ Practical steps to improve your score

🧾 What is a CIBIL Score? (Simple Explanation)

A CIBIL score is a 3-digit number (300–900) that represents your creditworthiness.

It reflects:

- Your repayment behavior

- Your financial discipline

- Your risk level as a borrower

👉 Higher score = Higher trust from lenders

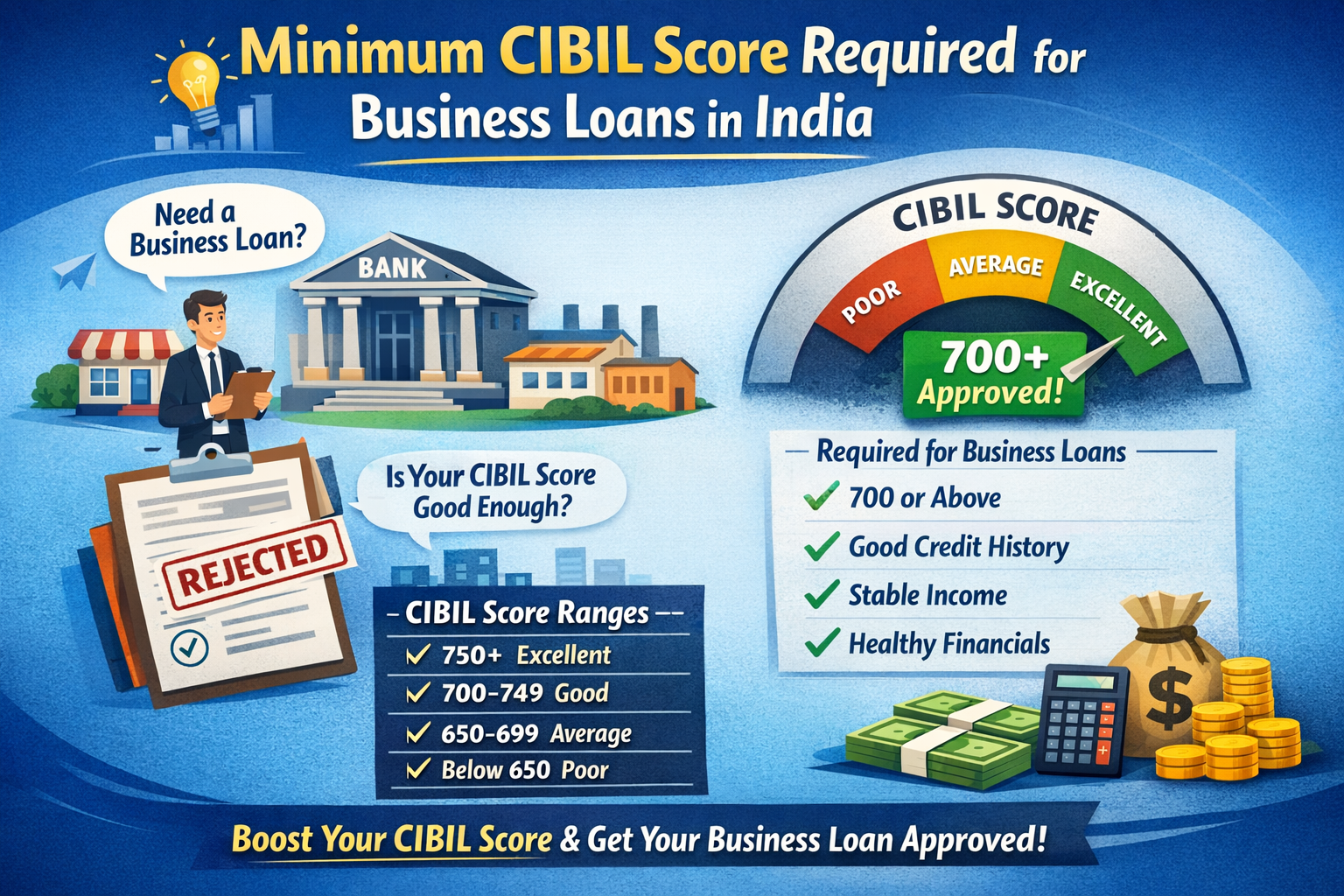

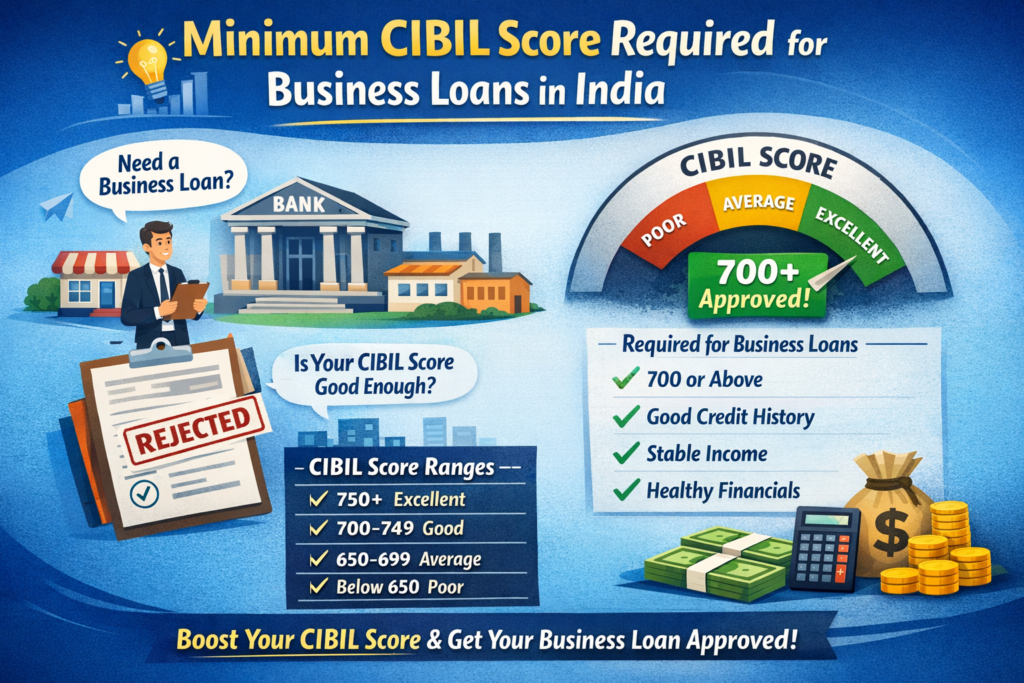

🏦 Minimum CIBIL Score Required for Business Loans

Score Range and Loan Impact:

| CIBIL Score Range | Approval Chances | Interest Rate |

| 750 – 900 | Excellent | Lowest |

| 700 – 749 | Good | Moderate |

| 650 – 699 | Average | High |

| 600 – 649 | Low | Very High |

| Below 600 | Very Difficult | Mostly Rejected |

🔍 What Do Lenders Check Apart from CIBIL Score?

CIBIL score is important, but lenders also evaluate:

✔ Credit History

- Past repayment behavior

- Any defaults or delays

✔ Business Stability

- Years in operation

- Business performance

✔ Income & Cash Flow

- Regular income

- Bank statements

✔ Existing Liabilities

- Current loans or EMIs

✔ Collateral (for secured loans)

- Property or asset value

⚠️ Common Reasons for Low CIBIL Score

If your score is low, these may be the reasons:

- ❌ Late EMI or credit card payments

- ❌ Loan defaults or settlements

- ❌ High credit utilization (using 80–90% of limit)

- ❌ Multiple loan enquiries

- ❌ Unpaid old dues

- ❌ Errors in credit report

🛠️ How to Improve Low CIBIL Score (Step-by-Step)

✅ Step 1: Check Your Credit Report

- Identify errors or unknown accounts

✅ Step 2: Pay EMIs and Credit Cards on Time

- Avoid delays completely

- Set auto-debit

✅ Step 3: Reduce Credit Utilization

👉 Keep it below 30%

✅ Step 4: Clear Old Dues

- Resolve written-off or settled accounts

✅ Step 5: Avoid Multiple Loan Applications

- Too many enquiries reduce your score

✅ Step 6: Use Secured Credit

- Try FD-based credit cards

🚫 Common Mistakes to Avoid

- ❌ Settling loans instead of properly closing them

- ❌ Paying only minimum due

- ❌ Not checking credit report regularly

- ❌ Applying for multiple loans simultaneously

- ❌ Using full credit card limit

💡 Expert Tips (Pro Insights)

✔ Aim for a 750+ score for best loan deals

✔ Maintain a mix of secured and unsecured credit

✔ Keep a long credit history

✔ Separate business and personal finances

✔ Monitor your credit report regularly

📊 Real-Life Example

Ravi, a small business owner from Assam, had a CIBIL score of 620.

Problem:

- High credit card usage

- One loan marked as settled

Result:

- Business loan rejected

What he did:

✔ Reduced credit usage

✔ Paid EMIs on time

✔ Cleared settlement account

👉 Within 6 months, his score improved to 720

👉 Loan got approved successfully

🏁 Conclusion

Getting a business loan is not difficult — if your CIBIL score is strong.

👉 Key takeaway:

- 700+ is safe

- 750+ is ideal

Even if your score is low, it can be improved with the right strategy and discipline.

❓ FAQs (Frequently Asked Questions)

Q1. What is the minimum CIBIL score required for a business loan?

👉 A score of 700 or above is generally recommended.

Q2. Can I get a business loan with a 650 score?

👉 Yes, but with higher interest rates and limited options.

Q3. How can I get a loan with a low CIBIL score?

👉 You can try NBFCs or opt for secured loans.

Q4. How long does it take to improve CIBIL score?

👉 Usually 3–6 months with consistent effort.

Q5. Does personal CIBIL score matter for business loans?

👉 Yes, especially for proprietors and small businesses.

🚀 Call-To-Action

If your CIBIL score is low, your report has incorrect entries, or your loan applications are getting rejected, there’s no need to worry. CrediBoost Solutions Pvt. Ltd. can professionally analyze and help improve your credit profile.

👉 Get your FREE consultation today and take control of your credit score!

📞 Call/WhatsApp: 8099690448 / 7086962101

🌐 Website: crediboost.com

Contact Number – 8099690448 / 7086962101

Address – C/O Sri Nagendra Borma, Hatilong, Near Maruti Suzuki Arena, North Lakhimpur, Assam – 787031

Email – support@crediboost.in

CIN NUMBER – U66190AS2025PTC027785

👉 Contact now and increase your chances of business loan approval!