Introduction: The Biggest Misunderstanding About Credit Score

Many people in India believe:

👉 “I have never taken a loan, so my credit score must be good.”

It sounds logical—but it is not true.

In reality, people with no loan history often face:

- Loan rejection

- Credit card rejection

- “No credit history found” issues

👉 The problem is not bad credit—it is no credit history.

👉 Good news:

In this guide, you will learn:

- Whether no loan means a good credit score

- How credit score actually works

- Why banks reject people with no credit

- How to build your credit score from zero

Featured Snippet Answer (Quick Summary)

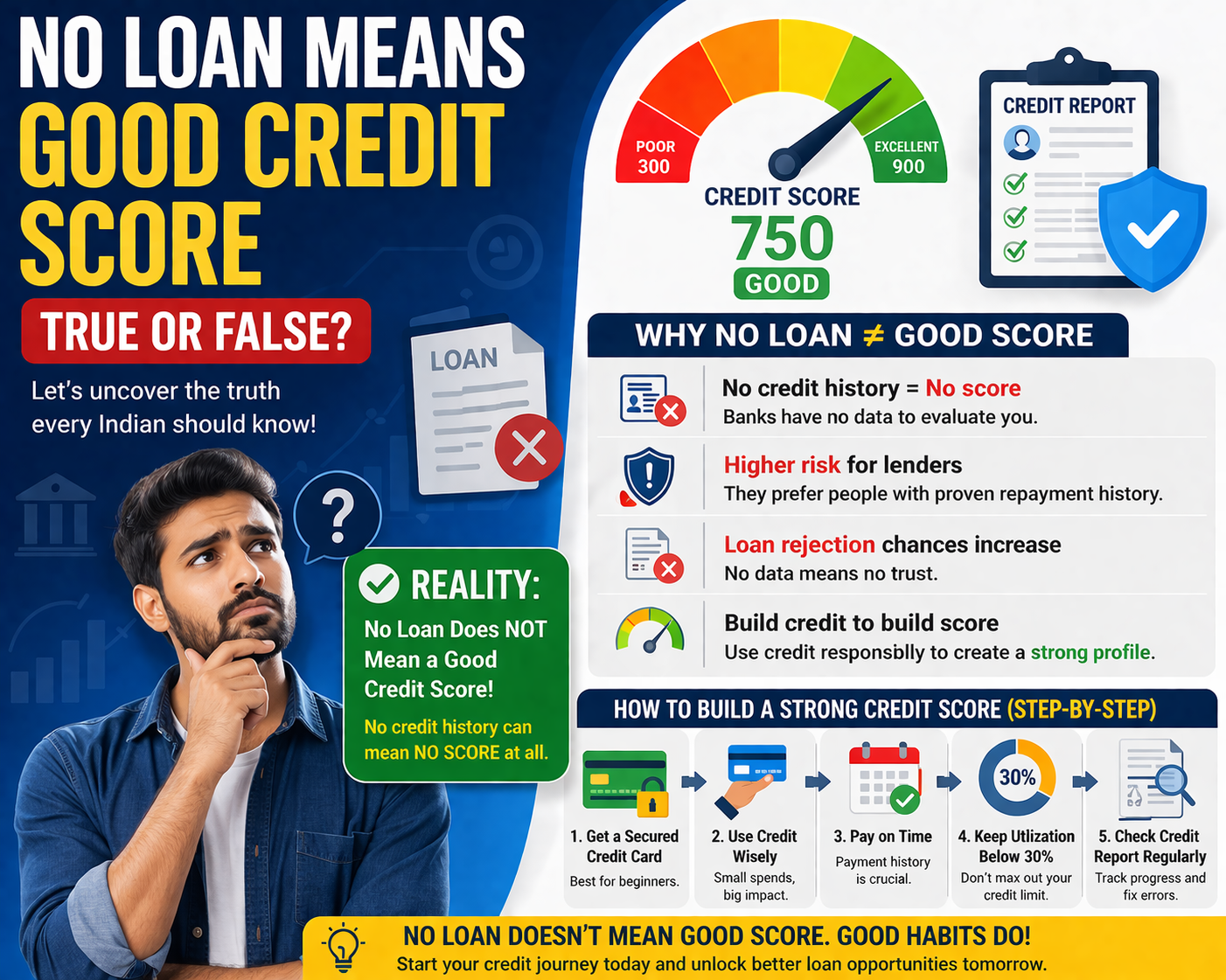

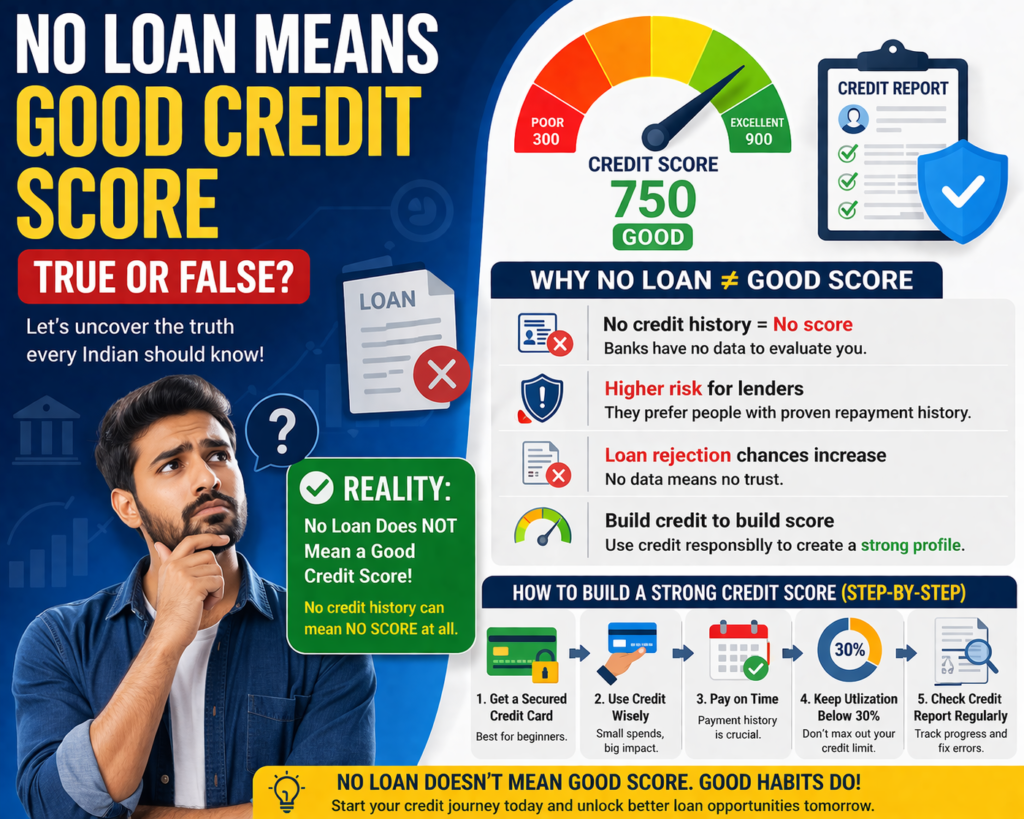

No, having no loan does not mean a good credit score. Without any credit activity, you may not have a credit score at all. To build a strong CIBIL score, you need to use credit responsibly and maintain a good repayment history.

What is a Credit Score? (Simple Explanation)

A credit score (CIBIL score) is a 3-digit number between 300 and 900 that shows how reliable you are with credit.

Credit Score Range:

- 750+ → Excellent

- 700–750 → Good

- 650–700 → Average

- Below 650 → Poor

👉 Banks use this score to:

- Approve loans

- Decide interest rates

No Loan Means Good Credit Score – True or False?

❌ Answer: False

Why It’s False

If you have never taken a loan or used a credit card:

👉 You have no credit history

👉 Without history:

- You may have no credit score

- Or a very low score

👉 Banks cannot judge your repayment behavior.

Why People Believe This Myth

- Fear of loans

- Lack of financial awareness

- Wrong advice from others

- Misunderstanding of credit system

What Happens When You Have No Loan History

1. No Credit History

- No record of repayment

2. No Credit Score

- You may be marked as “New to Credit”

3. Higher Risk for Lenders

- Banks prefer people with proven repayment history

4. Higher Chances of Loan Rejection

- No data = no trust

Real-Life Example (Indian Scenario)

Case 1: No Credit User

- Never used a credit card or loan

👉 Result:

- Loan rejected

- No credit score

Case 2: Smart Credit User

- Uses credit card regularly

- Pays on time

- Keeps usage low

👉 Result:

- Score: 780+

- Easy loan approval

👉 Lesson:

Avoiding credit does not help—using it wisely does.

What Actually Affects Your Credit Score

1. Payment History (35%)

- On-time payments increase score

2. Credit Utilization (30%)

- Keep usage below 30%

3. Credit Age (15%)

- Older accounts improve score

4. Credit Mix (10%)

- Different types of credit

5. Hard Enquiries (10%)

- Too many applications reduce score

Step-by-Step Guide: How to Build Credit Score from Zero

Step 1: Start with a Secured Credit Card

- Based on Fixed Deposit

- Easy approval

Step 2: Use Credit Regularly

- Make small purchases

Step 3: Pay Bills on Time

- Most important factor

Step 4: Maintain Low Credit Utilization

- Keep below 30%

Step 5: Avoid Multiple Loan Applications

- Apply only when needed

Step 6: Check Your Credit Report

- Track progress

- Fix errors

Common Mistakes to Avoid

❌ Avoiding credit completely

❌ Not building credit history

❌ Using full credit limit

❌ Missing payments

❌ Applying for multiple loans

Expert Tips (Pro Insights)

✔ Start building credit early

✔ Use credit card responsibly

✔ Monitor your credit regularly

✔ Maintain financial discipline

✔ Focus on long-term habits

Best Ways to Build Credit Safely

1. Secured Credit Card

- Safe and beginner-friendly

2. Small Loan

- Helps build repayment history

3. Add-on Credit Card

- From family member

FAQs (Frequently Asked Questions)

1. Can I have a good credit score without a loan?

No, you need credit activity to build a score.

2. What happens if I never take a loan?

You may not have a credit score.

3. Is no credit better than bad credit?

Yes, but still not ideal for loan approval.

4. How can beginners build credit score?

- Use secured credit card

- Pay on time

5. How long does it take to build credit score?

Usually 3 to 6 months.

Conclusion: Use Credit Smartly, Not Fearfully

Let’s make it clear:

👉 No loan does NOT mean a good credit score

👉 It may actually mean no credit score at all

The key is not avoiding credit—it is managing it responsibly.

👉 Start small, stay disciplined, and build your credit step by step.

🚀 Take Action Now – Improve Your CIBIL Score

Agar aapka CIBIL score low hai, report me galat entry hai, ya loan reject ho raha hai, to tension lene ki zarurat nahi hai. CrediBoost Solutions Pvt. Ltd. aapki credit profile ko professionally analyze karke improve karne me help karta hai.

👉 Aaj hi apna free consultation lein aur apna CIBIL score better banaye.

📞 Call/WhatsApp: 8099690448 / 7086962101

🌐 Website: crediboost.com

Contact Number – 8099690448 / 7086962101

Address – C/O Sri Nagendra Borma , Hatilong , Near Maruti Suzuki Arena , North Lakhimpur , Assam -787031

Email – support@crediboost.in

CIN NUMBER – U66190AS2025PTC027785