Introduction: Is Your Loan Getting Rejected Again and Again?

If your loan applications are getting rejected or your credit score has suddenly dropped, there is a high chance that your CIBIL report shows a “Written-Off Account.”

Many people misunderstand this term and assume their loan is “closed” or “forgiven.”

But the reality is very different—and more serious.

👉 A written-off account is one of the most damaging entries in your credit report.

In this detailed guide, you’ll learn:

- What a written-off account actually means

- Why it happens

- Its impact on your credit score

- And most importantly, how to fix it

📌 Featured Snippet (Quick Answer)

A Written-Off Account in CIBIL means that the lender has declared your loan as a loss in their records due to non-payment for a long period (usually 180+ days). However, the borrower is still legally obligated to repay the amount, and it severely damages the credit score.

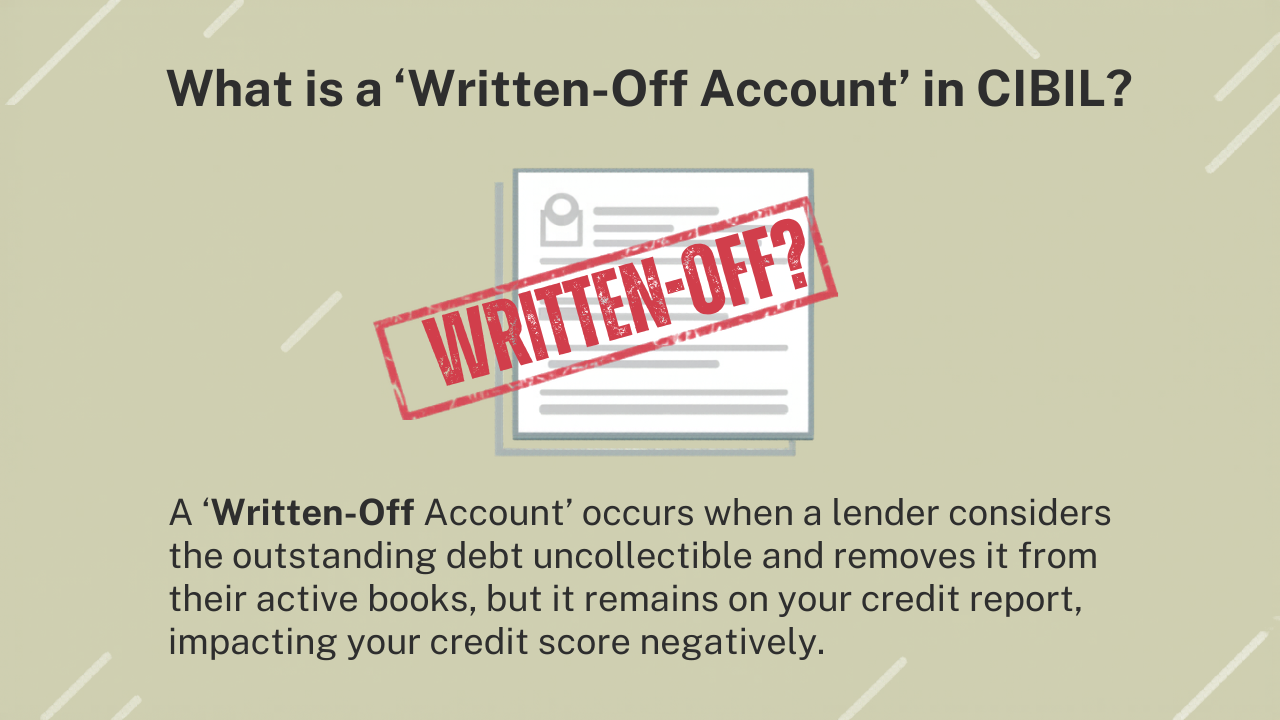

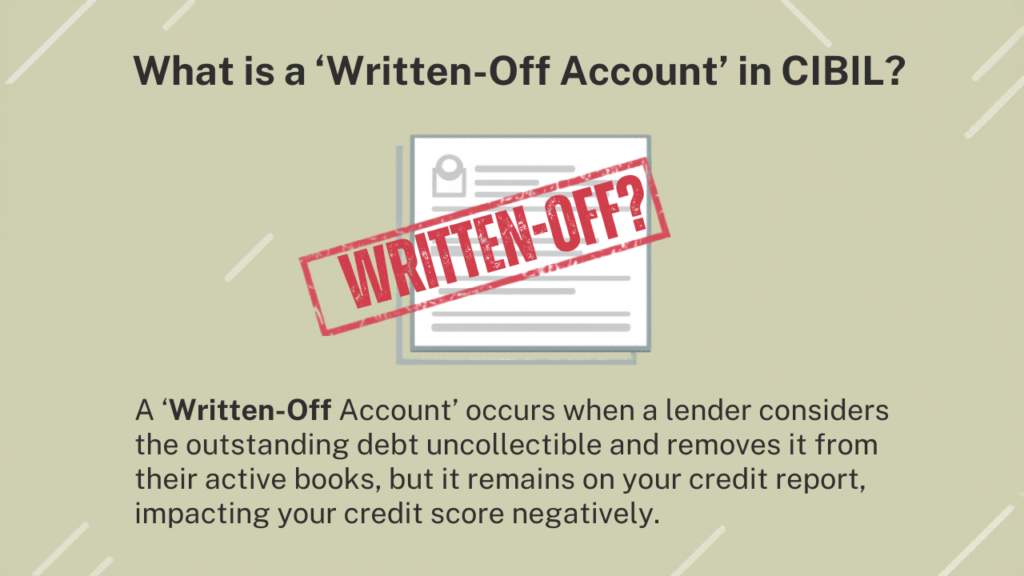

What is a Written-Off Account in CIBIL? (Simple Explanation)

When a borrower fails to repay a loan or credit card dues for a long time (typically more than 6 months), the bank or NBFC marks the account as “Written-Off.”

Simple Example:

Suppose you took a personal loan of ₹1,00,000 and stopped paying EMIs. After continuous default for several months, the lender classifies the account as “Written-Off.”

👉 Important Points:

- The loan is NOT forgiven

- You still owe the money

- Recovery actions can continue

Types of Written-Off Accounts

1. Technical Write-Off

- Loan is removed from the lender’s active books

- Recovery process still continues

2. Settlement / Partial Write-Off

- Borrower negotiates and pays a reduced amount

- Account is marked as “Settled” instead of “Closed”

👉 Both cases negatively impact your CIBIL score.

Main Reasons / Causes of Written-Off Accounts

Here are the most common reasons:

- Failure to pay EMIs regularly

- Financial crisis (job loss, business loss)

- Ignoring credit card dues

- Taking multiple loans beyond repayment capacity

- Intentional default

- Poor financial planning

Impact of Written-Off Account on CIBIL Score

A written-off account has a severe negative impact on your credit profile.

🔴 Key Effects:

- Credit score can drop by 100–200 points

- Loan approvals become extremely difficult

- Credit card approvals get rejected

- Lenders consider you a high-risk borrower

👉 This record can stay in your report for up to 7 years

Real-Life Example (Relatable Case)

Rahul had a credit card with ₹80,000 outstanding. Due to financial issues, he stopped paying.

After 6 months:

- Account was marked “Written-Off”

- His score dropped from 780 to 580

- Every loan application started getting rejected

Later, he cleared dues and improved his credit with proper guidance.

Solutions / Actionable Steps (Step-by-Step)

If your account is written-off, don’t panic. You can still improve your situation.

Step 1: Check Your CIBIL Report

- Identify which accounts are written-off

Step 2: Repay the Outstanding Amount

- Full payment is the best option

- Or negotiate a settlement if necessary

Step 3: Get NOC (No Objection Certificate)

- Always collect NOC after payment

Step 4: Request Status Update

- Ask lender to update status to “Closed” or “Settled”

Step 5: Build Positive Credit History

- Use secured credit cards

- Pay EMIs on time

- Keep utilization low

Step 6: Take Professional Help

- Experts can guide you faster and more effectively

Common Mistakes to Avoid

- Thinking written-off means loan is waived

- Ignoring recovery notices

- Not taking NOC after payment

- Repeating the same financial mistakes

- Not checking credit report regularly

Expert Tips / Pro Insights

- Always pay EMIs before the due date

- Maintain credit utilization below 30%

- Keep an emergency fund (3–6 months expenses)

- Avoid multiple loans at the same time

- Monitor your credit report regularly

👉 Pro Tip: Fixing a written-off account should be your top priority before applying for any new loan.

Frequently Asked Questions (FAQs)

1. Does written-off mean loan is forgiven?

No, you are still legally required to repay the loan.

2. Can a written-off account be removed?

It cannot be removed directly, but it can be updated after repayment.

3. How long does it stay in CIBIL?

Up to 7 years.

4. Is settlement a good option?

Only if full repayment is not possible, but it still affects your score negatively.

5. Can I get a loan after a written-off account?

Difficult, but possible after improving your credit profile.

Conclusion: What Should You Do Now?

A written-off account is a serious issue—but it is not permanent. With the right steps and discipline, you can rebuild your credit profile and regain financial trust.

👉 Remember:

Ignoring the problem will worsen it. Taking action will solve it.

🚀 Call-To-Action

If your CIBIL score is low, your report has incorrect entries, or your loan applications are getting rejected, there’s no need to worry. CrediBoost Solutions Pvt. Ltd. helps you professionally analyze and improve your credit profile.

✔ Expert analysis

✔ Personalized solutions

✔ Fast-track credit improvement strategies

👉 Get your FREE consultation today and start improving your CIBIL score now.

📞 Call/WhatsApp: 8099690448 / 7086962101

🌐 Website: crediboost.com

Contact Number – 8099690448 / 7086962101

Address – C/O Sri Nagendra Borma, Hatilong, Near Maruti Suzuki Arena, North Lakhimpur, Assam – 787031

Email – support@crediboost.in

CIN NUMBER – U66190AS2025PTC027785

Don’t wait—take control of your financial future today!